Resist the itch to switch

Day after day we are bombarded by the media and at the moment, we are seeing nothing but bad news. Coverage of the share market is full of headlines with words such as “plunge”, “recession” and “loss” repeated over and over again.

You know you shouldn’t, but just can’t help it; you take a glimpse at your KiwiSaver balance. Gulp! The gains from the previous one or two years are gone.

Your first instinct is to stem the drop, to take some control of the situation. You think, “I’m not going to sit around and let this happen to me. I’m going to switch from the growth to the conservative fund.” But to avoid sounding too radical, you console yourself by thinking, “When things get better, I’ll switch back.”

This scenario is unfolding in real time. On 26 March one of the nation’s largest KiwiSaver supervisors commented that “switching,” an industry term for changing your KiwiSaver asset allocation, had increased over 1000% from the previous week. (1)

KiwiSaver is the quintessential long-term investment strategy. Given the average age of the New Zealand workforce is around 43 (2), most KiwiSaver investors will have a time horizon of many decades, and some longer than 50 years. Given this time horizon, what could possibly be the reason investors are looking to make changes right now? In a word, “fear.”

Hindsight is a wonderful thing. With the benefit of hindsight, we can evaluate if there is any benefit to switching portfolios in the middle of a crisis.

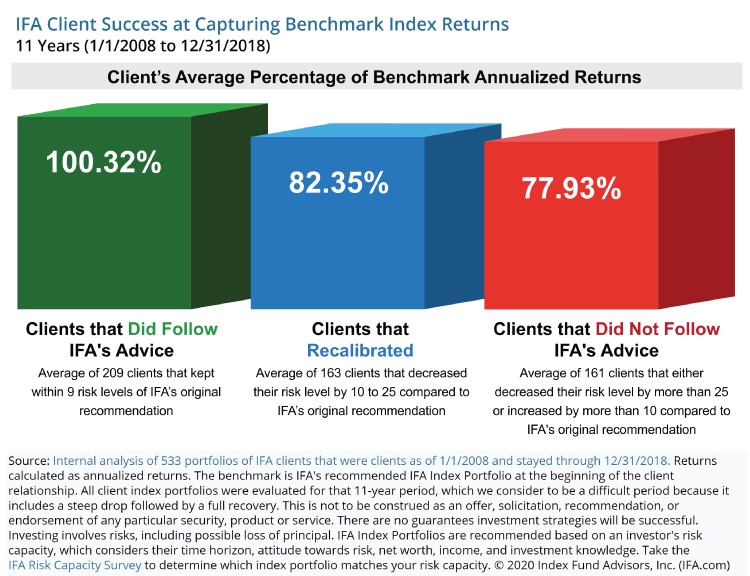

One of the best studies comes from a financial advisory firm in the USA, Index Funds Advisors (IFA). They analysed the returns of 533 existing client strategies in place as of 1 January 2008 and analysed how their switching decisions during the global financial crisis (GFC) affected their long-term returns.

IFA categorised its clients into three buckets:

- Category 1 (green bar), were those that followed advice and kept their recommended portfolio.

- Category 2 (blue bar), were those that recalibrated, generally by decreasing their risk levels by 10% to 25% (e.g. moving from growth to balanced).

- Category 3 (red bar) , were those that changed their portfolio allocation by more than 25% (e.g. moving from growth to conservative).

So, how successful were those three client categories in capturing the return of the markets over the subsequent 10 years? Clients that took advice and followed it received 100.32% of the return achieved by their original benchmark portfolio. Clients that reduced risk received only 82% of the return achieved by their original benchmark portfolio. Clients in the third category only received 78% of the return achieved by their original benchmark portfolio.

In other words, in the 10 years since the GFC, switching resulted in a significant but altogether avoidable destruction of wealth.

This isn’t theory. These were real clients achieving (or not achieving) actual returns.

Switching due to fear is the equivalent of the common English phrase “to close the stable door after the horse has bolted.” In other words, implementing a solution that won’t solve the problem. But in the case of switching KiwiSaver allocations, the solution is worse than bolting a gate because it could bring real harm. It has similar logic to accepting amputation as a solution to a sprained ankle.

Of course, when we find ourselves struck by fear, we may not stop to consider the best path to recovery. We are just trying to make the pain stop.

However, we encourage you to “resist the itch to switch.” Given a time horizon of decades rather than days, it’s your best chance to achieve the long term outcomes you have planned for, and the reason you invested in the first place.

Ben Brinkerhoff

Head of Adviser Services, Consilium