What REALLY adds value when you choose a KiwiSaver scheme?

We’ve all seen them, advertisements that go something along the lines of, “XYZ Scheme is the highest performing KiwiSaver fund for the last 5 years”.

The implication of the advertisement is simple; recent performance is the singular piece of information most important in selecting your KiwiSaver fund. But is it?

With 15 years of KiwiSaver returns data now available, we can start to zero in on what really adds value when you choose a KiwiSaver scheme. Hint, it’s not recent returns.

Looking at the last 15 years of KiwiSaver returns data, this article will ask three questions:

- Does switching to a different KiwiSaver manager based on recent past returns help or hurt your subsequent performance?

- Does switching to a different KiwiSaver manager based on fees help or hurt your subsequent performance?

- What’s the impact of allocations to shares, bonds and cash on overall KiwiSaver performance?

For the purposes of this article, we will remain ambivalent about the other issues that might be considered before changing KiwiSaver funds/providers such as convenience, service, quality, and readability of information, etc. These do matter, but for now, let’s focus on the three questions posed above.

First, does changing to a different KiwiSaver manager based on recent past returns really lead to better returns in the future?

To assess this, we’ll look exclusively at switches from within the Morningstar category 'Aggressive Allocation' which includes KiwiSaver funds that have a much higher proportion in shares than bonds and cash. It’s the natural category to use when overall performance is the key metric. We are also limiting our analysis to allocation funds where one fund is diversified across many different asset types.

In this analysis we are not looking at switches between risk levels, for example switching from an Aggressive to a Conservative fund.

To evaluate our question, we will look at four generic behaviours an investor might exhibit:

Holding: An investor chooses a random fund at the start and never changes.

Chasing: An investor looks at the last 12 months of cumulative returns and switches to one of the top 10% of best performing funds every 12 months as if trying to chase good returns.

Avoiding: An investor looks at the last 12 months of cumulative returns and switches to one of the bottom 10% of worst performing funds every 12 months as if trying to find funds more likely to bounce back.

Random: An investor randomly selects a new fund every 12 months.

If this trial is run 100 times, which of the four behaviours listed above will, on average, end up with the highest balance? Intuitively the 'Chasing' category might seem most appealing. Here you know who the best recent performers are, so you’re not selecting entirely at random. And surely having this information means it’s more likely you will pick a winner, right?

In the same vein, you might think 'Avoiding' could lead to the highest balance. But how could choosing a fund based on selecting from the worst recent performers be a good approach?

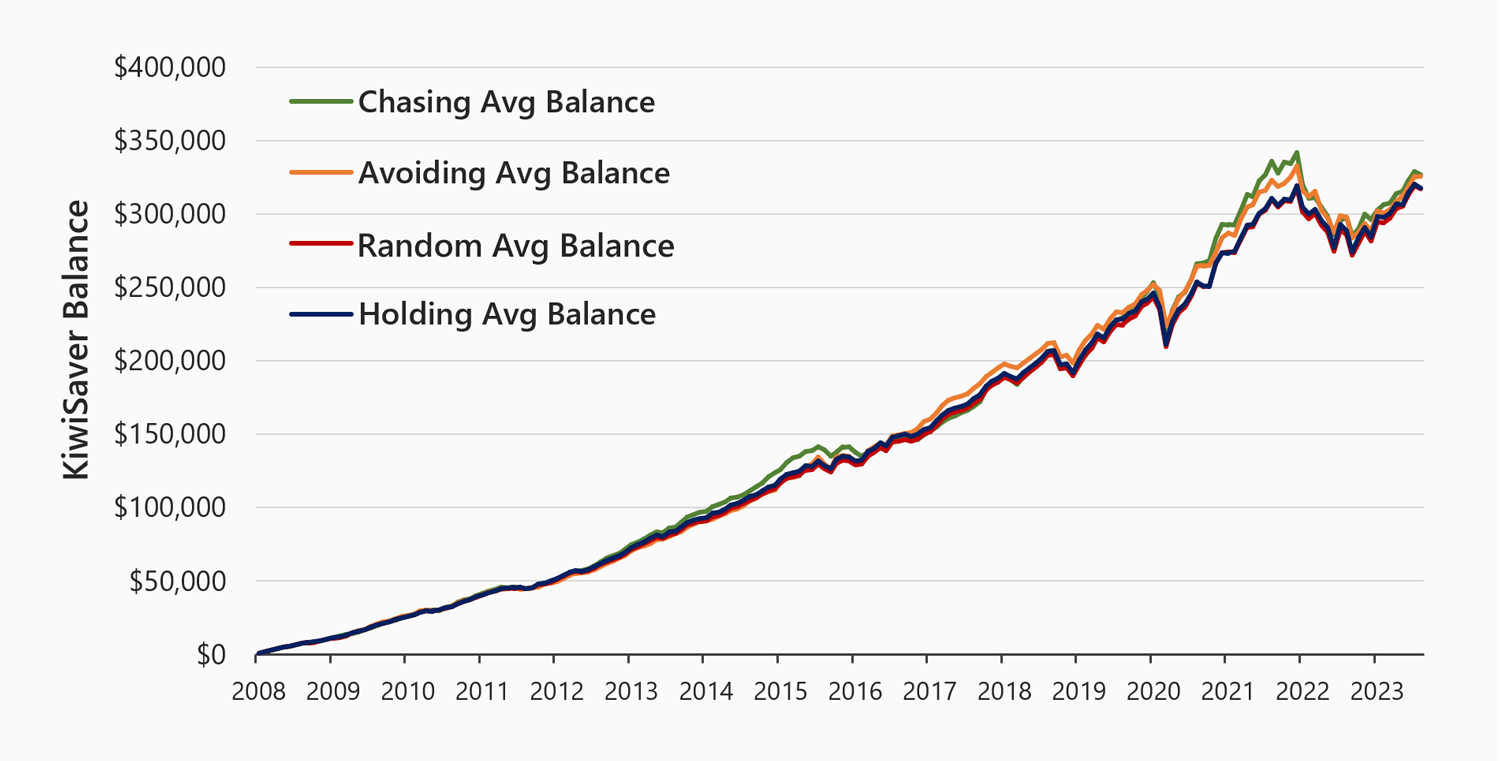

Well, here’s the results.

This chart, as the others in the article assume that at the start of each month, investors add a constant amount of money (in this case $1,000) into their portfolios. Trials begin January 2008 and end August 2023.

In the chart above, each line represents the average overall growth of wealth (including from regular savings) delivered by each of the four behaviours, ‘holding’, ‘chasing’, ‘avoiding’ and ‘random’ for an investor contributing $1,000 a month from January 2008 to August 2023.

So, what inferences can we draw from this chart about investing based on past performance? Well, the first thing you observe is that the lines are all on top of each other. This suggests that chasing performance, avoiding performance, holding or selecting at random doesn’t really add or detract from returns relative to any other strategy on average.

From 2008 to 2023, you get an almost identical balance ($326,112) from selecting amongst the bottom 10% of recent performers as you get from selecting a manager amongst the top 10% ($326,767). The adage, "Past performance is no guarantee of future results” rings very true here, because recent winners do not appear to become persistent winners.

The implication is that investors should be sceptical of any advertising encouraging them to switch schemes based on recent good performance. Performance chasing based on recent returns does not appear to add value when you are choosing between KiwiSaver funds.

The second question is, does switching to a different KiwiSaver manager based on fees lead to better or worse returns in the future?

As in the previous example, we need to create two categories and compare the results.

Fee Avoider: An investor chooses a new fund every 12 months, by randomly selecting from within the 10% of lowest cost schemes available. In other words, this is an investor that is highly sensitive to the level of fees.

Fee Chaser: An investor chooses a new fund every 12 months by randomly selecting from within the 10% of highest cost schemes available. By contrast, this investor doesn’t put much emphasis on fees (while this isn’t an approach we would expect to see very often, it does create a useful contrast to our fee avoider).

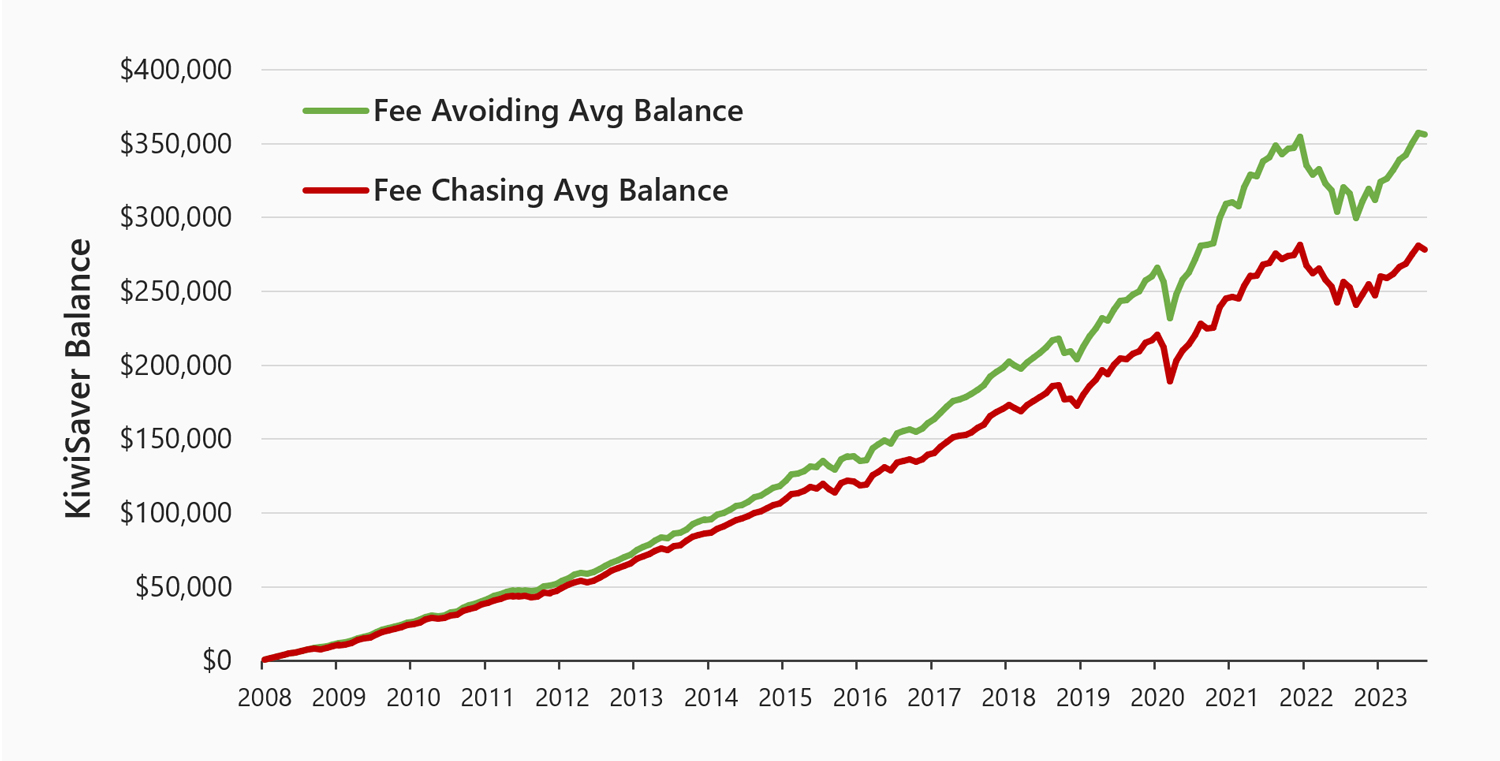

Again, we run 100 trials of each strategy and compare the average results. The findings are equally as fascinating as those in the previous example.

The average fee avoiding strategy is the bold green line and the average fee chasing strategy is the bold red line. Depending on the actual low cost or high cost strategies selected, the outcome experienced may have differed from the average outcome depicted above. Trials begin January 2008 and end August 2023.

In contrast to the previous chart, we discover that you are likely to end up with a meaningfully higher balance if you ‘avoid’ rather than ‘chase’ fees. Here the average balance for fee avoiders is $356,210 which is much higher than fee chasers ($278,176) and also higher than the ending balance of any of our previous performance-based strategies. For most things in life, you get what you pay for. However, with KiwiSaver, you get (to keep) what you don’t pay for (in investment management fees).

The inference from these first two trials is that while recent performance does not add value when choosing a KiwiSaver fund, selecting a fund from a scheme with lower overall fees does add value.

There are some caveats to the above analysis. Both trials outlined above have assumed investors are in an 'Aggressive Allocation' as defined by Morningstar Investment Research. However, according to a recent PWC report on KiwiSaver during Covid, only a small fraction of investors actually do have an aggressive KiwiSaver allocation.

We also assume that investors never move to a lower risk allocation or reduce contributions due to volatile markets, but some do. Unfortunately, these decisions are often driven by emotion and made at the wrong time. It can’t be stated enough, good investor behaviour matters more than either of our tests about performance or fees.

The last caveat is that this analysis defines 'success' as ending up with the highest balance in your KiwiSaver account. But that’s not always a good definition of success. Success is probably better defined as being able to confidently enter retirement with all the assets you need, both inside and outside KiwiSaver. Whatever your ending KiwiSaver balance, many people would consider having peace of mind about retirement a tremendous success.

To achieve that peace of mind you should consider getting professional advice. Based on your specific circumstances, good advice might suggest you hold a KiwiSaver with lower investment costs and a more aggressive allocation. That’s why recent KiwiSaver entrants like the KiwiWRAP KiwiSaver Scheme are an important option.

The KiwiWRAP KiwiSaver scheme encourages independent advice on your KiwiSaver investment allocations. Because the adviser is paid by you, and they have freedom to select from over 400 fund and investment options rather than be limited to just one fund, from one scheme provider, your KiwiSaver portfolio can be tailored for you. This wide investment choice enables you and your adviser to meaningfully consider your overall objectives around a secure retirement and the scope to reduce investment management fees in the process.

This brings us to the final question, what’s the impact of your allocation to shares, bonds and cash on overall KiwiSaver performance?

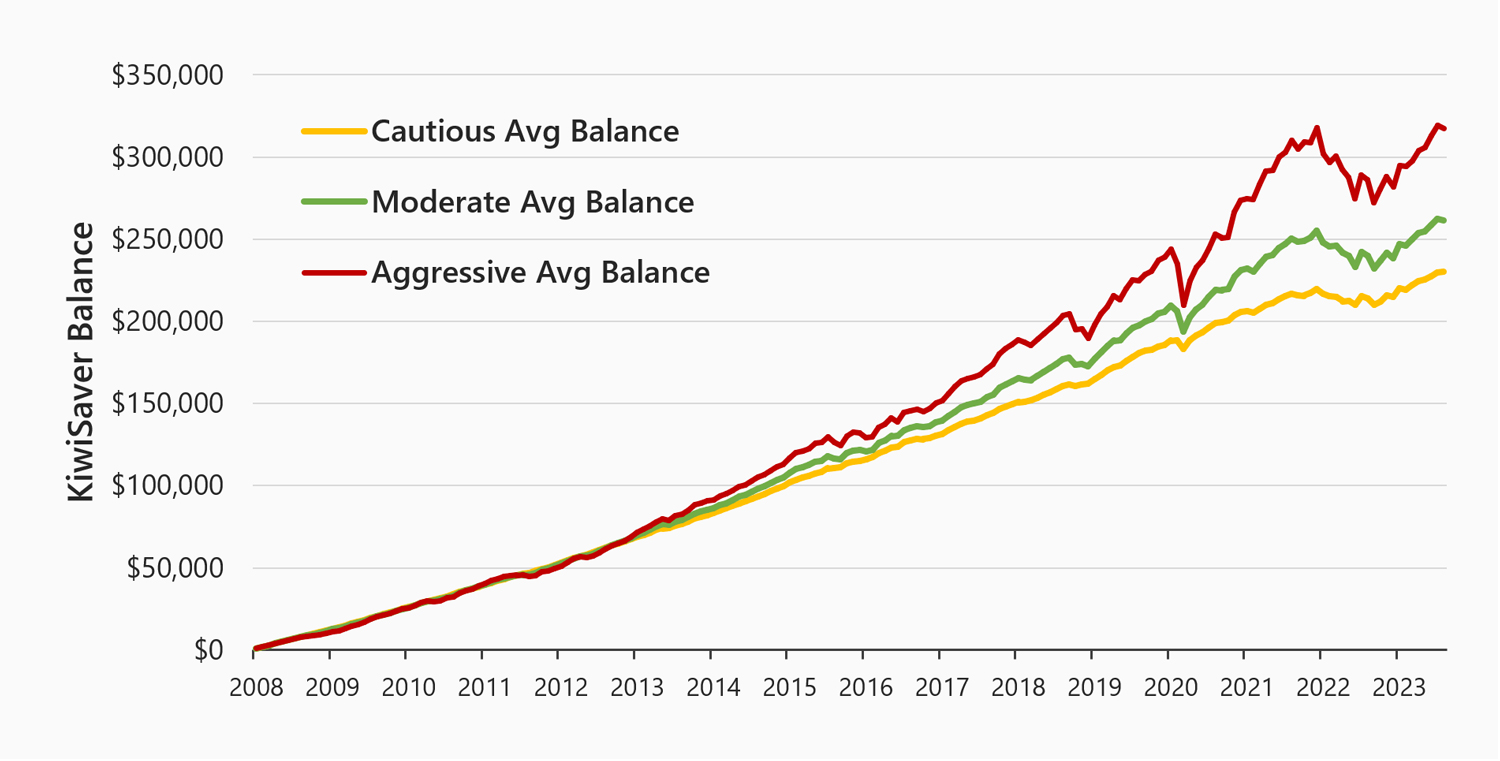

To address the impact of advice and asset allocation decisions, we ran a third trial where we selected randomly between schemes Morningstar defined as Aggressive, Moderate and Cautious. For clarity, an Aggressive allocation invests mostly in shares, a Moderate allocation invests about 50% in shares and a Cautious allocation invests mostly in cash and bonds.

The results are shown below.

This test is akin to the 'random' selection from our first test. It assumes an investor selects a scheme at random within each category every 12 months. The trial is run 100 times and above we display the average results. Trials begin January 2008 and end August 2023.

The average return of a randomly selected Aggressive fund ($317,330) does much better over time than a randomly selected Moderate ($261,586) or Cautious fund ($230,097).

You may ask why it takes several years to see a divergence in the performance. This is because early on the regular cash contributions to the scheme have by far the largest impact when your balance is small. Over time, as KiwiSaver balances grow, investment performance starts to have a more meaningful impact and outcomes diverge. This is why advice matters more once your KiwiSaver balance grows.

The implications of this research are clear:

☑️ Choose a fund with the most aggressive allocation appropriate for your circumstances and consider getting advice so your assets are working to achieve your overall objectives for a comfortable and secure retirement.

☑️ Make low investment management fees, rather than recent returns, a more important factor in choosing your KiwiSaver scheme.

☑️ Don’t chase performance or worry if someone else was in the best performing fund over some recent time-period. Chasing returns probably won’t add value and might just create unrealistic expectations that lead to making worse decisions down the road.

Overall, consider professional advice as it is more likely to deliver three key value-adds:

- Help you to be more comfortable selecting a more aggressive allocation appropriate for your age and circumstances and allocating to a fund with lower overall investment management fees.

- Assist you in having more discipline to continue to hold that allocation through volatile markets.

- Provide you with the peace of mind by having a clear strategy in place to fully fund your ideal retirement.

If you get this sort of value from advice, then you’ll end up with a far better outcome than most investors will achieve on their own.